All Categories

Featured

Table of Contents

There is a 3 year redemption period for most homes marketed at the tax lien sale and throughout that time, the building still belongs to the evaluated owner. Extremely few home tax obligation liens actually go to action.

The rate of interest on tax obligations acquired at the tax obligation lien sale is nine portion factors above the discount rate paid to the Reserve bank on September 1st. The rate on your certificate will remain the very same for as long as you hold that certification. The price of return for certifications offered in 2024 will certainly be fourteen percent.

The certificates will certainly be held in the treasurer's office for safekeeping unless otherwise instructed. If the tax obligations for ensuing years come to be delinquent, you will be notified around July and provided the opportunity to recommend the taxes to the certifications that you hold. You will certainly get the exact same rate of interest on succeeding tax obligations as on the initial certificate.

The redemption period is 3 years from the date of the initial tax sale. You will obtain a 1099 kind revealing the quantity of redemption interest paid to you, and a duplicate will certainly also be sent to the Internal revenue service.

Spending in tax obligation liens and deeds has the possible to be quite rewarding. It is also feasible to invest in tax obligation liens and deeds with less funding than may be needed for other investments such as rental residential or commercial properties.

Certificate In Invest Lien Tax

Tax obligation liens might be levied on any type of kind of residential property, from raw land to homes to commercial homes. The policies surrounding the kind of lien and just how such liens are released and redeemed differs by state and by area. There are two main classes, tax liens and tax actions. A tax lien is issued quickly once they residential or commercial property owner has actually stopped working to pay their taxes.

Such liens are then offered for sale to the public. An investor purchases the lien, thus offering the community with the needed tax obligation revenue, and after that deserves to the residential or commercial property. If the homeowner pays their tax obligations, the capitalist normally gets interest which can be in the variety of 12-18%.

If the home is not retrieved, the investor might seize on the residential property. Tax obligation liens and deeds offer the opportunity for generous roi, possibly with reduced amounts of funding. While there are certain threat variables, they are reasonably reduced. Tax obligation lien investing is concentrated on the collection of passion and penalties (where readily available) for the tax obligation debt.

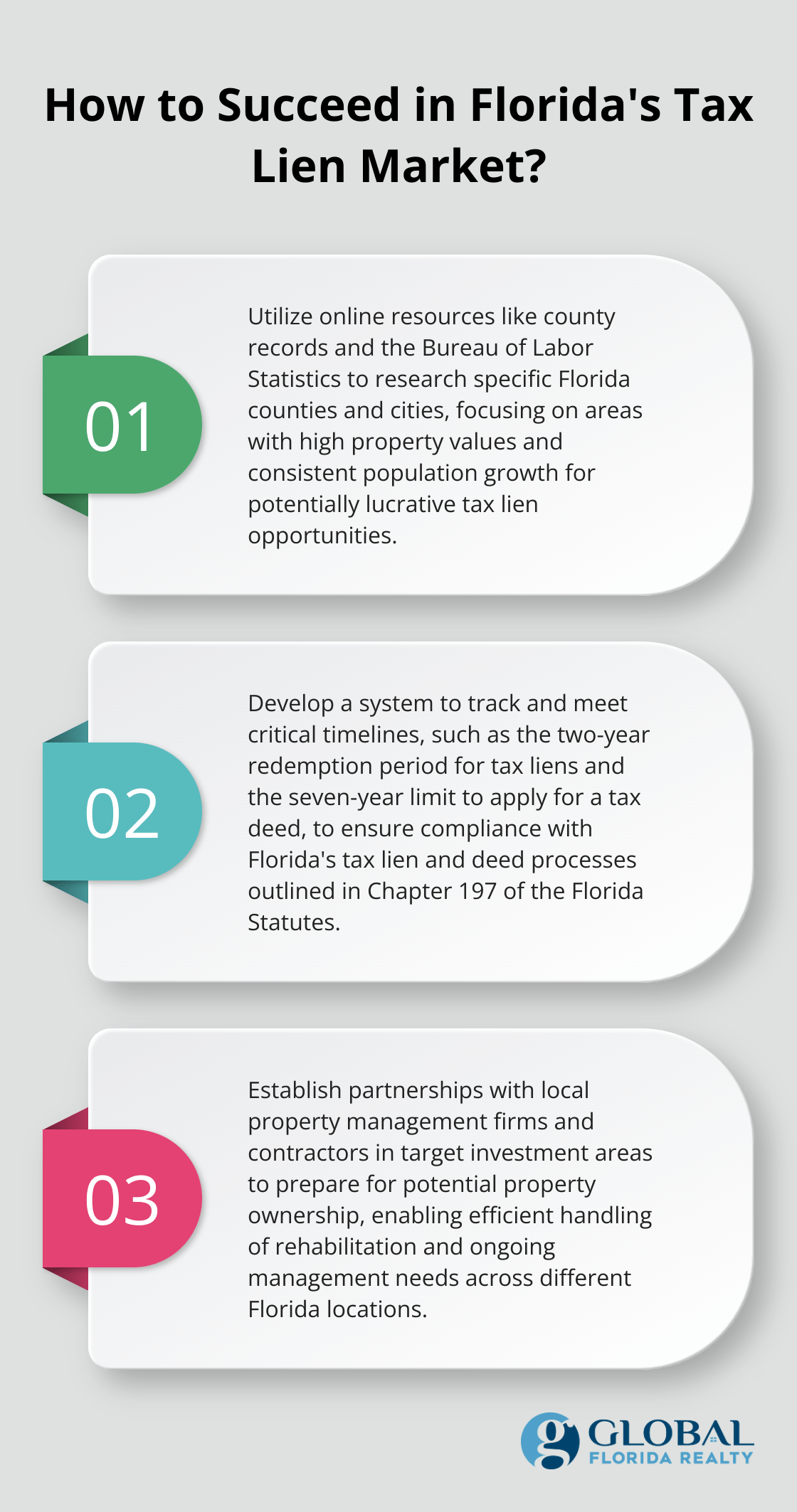

The process for spending differs by state and by area. Most liens and acts are cost auction, with some public auctions happening in-person at an area courthouse, and some taking place online. You will generally require to register ahead of time for such auctions and may be needed to put a down payment to get involved.

Investing In Real Estate Tax Liens

In some jurisdictions, unsold liens or deeds might be readily available up for sale "nonprescription" from the area staff's workplace or web site after an auction has been completed. Prior to getting involved in an auction, you will certainly want to perform research to determine those buildings you may be interested in and guarantee there are no issues such as other liens that may need to be worked out or problems with the home itself that may produce concerns if you were to take control of ownership.

This duration is implied to offer the residential property proprietor an opportunity to resolve their financial obligation with the exhausting authority. With a lien, redemption implies that your Individual retirement account or 401(k) will get a payday, with passion and any type of applicable charges being paid.

Tax lien and deed investing is an area where checkbook control is a must. You need to be able to provide funds directly on brief notice, both for a down payment which has to be signed up in the strategy entity name, and if you are the winning bidder. With a Checkbook Individual Retirement Account LLC or Solo 401(k), you can directly make such repayments from your strategy account without delays or third event fees.

If you make a deposit and are not effective in bidding at auction, the down payment can just be returned to the strategy account without problem. The a number of days processing delay that comes with working directly via a self-directed individual retirement account custodian simply does not work in this area. When investing in tax obligation liens and acts, you should ensure that all tasks are carried out under the umbrella of your strategy.

All costs connected with tax lien investing have to originate from the plan account straight, as all income created should be deposited to the strategy account. tax lien certificates investing. We are typically asked if the plan can pay for the account holder to go to a tax obligation lien training course, and suggest against that. Even if your investing activities will be 100% with your plan and not involve any individual investing in tax liens, the IRS might consider this self-dealing

Best Books On Tax Lien Investing

This would additionally hold true of getting a property through a tax act and afterwards holding that residential property as a service. If your method will include acquiring properties just to transform about and re-sell those homes with or without rehabilitation that can be deemed a dealer task. If performed regularly, this would subject the individual retirement account or Solo 401(k) to UBIT.

As with any type of financial investment, there is danger connected with buying tax liens and actions. Financiers ought to have the economic experience to determine and recognize the risks, execute the needed diligence, and correctly administer such investments in conformity internal revenue service regulations. Protect Advisors, LLC is not a financial investment consultant or company, and does not advise any kind of details investment.

The info above is academic in nature, and is not meant to be, neither needs to it be construed as supplying tax obligation, lawful or financial investment suggestions.

Tax Lien Investing Scam

6321. LIEN FOR TAX OBLIGATIONS. If any kind of individual liable to pay any type of tax forgets or declines to pay the same after need, the amount (consisting of any type of rate of interest, added quantity, enhancement to tax obligation, or assessable charge, together with any type of expenses that may accrue in enhancement thereto) will be a lien in support of the United States upon all home and rights to residential property, whether actual or personal, belonging to such individual.

Tax Lien Deed Investing

Division of the Treasury). Usually, the "individual reliant pay any type of tax obligation" described in section 6321 must pay the tax within ten days of the created notice and demand. If the taxpayer stops working to pay the tax within the ten-day duration, the tax lien arises immediately (i.e., by operation of legislation), and works retroactively to (i.e., develops at) the date of the assessment, also though the ten-day duration always ends after the assessment day.

A government tax obligation lien arising by law as defined above stands versus the taxpayer without any kind of more action by the government. The basic policy is that where 2 or even more creditors have competing liens against the same residential or commercial property, the financial institution whose lien was developed at the earlier time takes concern over the lender whose lien was refined at a later time (there are exceptions to this guideline).

{kind=link}

Table of Contents

Latest Posts

Unpaid Taxes On Homes For Sale

Sale Tax Property

Houses Up For Tax Sale Near Me

More

Latest Posts

Unpaid Taxes On Homes For Sale

Sale Tax Property

Houses Up For Tax Sale Near Me